The economic environment continued to remain somber

in the year 2012. After a sharp decline in the global growth

momentum in the year 2011 to 4.0 percent from 5.3 percent

in the year 2010, the global growth declined further to 3.2

percent in the year 2012, barely above the recessionary

growth of 3 percent. One of the key reasons for the growth

slowdown was sharp decline in the growth of emerging

economies during the year to 5.1 percent against the

growth of 6.3 percent in the year 2011.

Number of positive policy actions taken during the year,

especially by the key policy makers of the advanced

economies would likely help in arresting this slide. These

actions also address a few major concerns including

the threat of a euro area breakup and the possibility of

triggering the “fiscal cliff” in the US leading to its sharp

fiscal contraction. Timely policy actions after a leadership

change in European Central Bank (ECB) and in a few of the

Euro member countries have resulted in bringing stability

to the region’s debt and currency market.

The global economy remains well supported by the

exceptionally benign monetary policy by central banks of

most advanced economies. These policy actions include

Fed’s open ended third round of quantitative easing,

ECB’s commitment to do whatever it takes to preserve

the euro and Japan’s USD 1.4 trillion quantitative easing.

The interest rates in all these economies continue to be

at a record low and in May 2013, ECB further reduced its

interest rates by 25bps to a new record low of 0.5 percent.

Another positive factor was the resilience and better than

the expected growth of the US economy. Despite a sharp

slowdown and lower than the projected growth of almost

all major economies, US grew much faster at 2.2 percent

against the projected growth of 2.1 percent in April 2012.

The US economy has been consistently building on its

slow yet steady growth momentum and the unemployment

rate in the US declined to a four year low of 7.6 percent in

April 2013.

Going forward, while there are several downside risks

that can derail the global growth momentum, the global

GDP growth is expected to increase slightly to 3.3 percent

during the year 2013 and more appreciably to 4.0 percent

in the year 2014.

INDIAN ECONOMY

During the fiscal 2012-13 (FY’13), Indian economic growth

continued to remain weak and the economy grew at a

decade low rate of less than 5 percent, much lower than

the estimated growth rate of 6.7 percent at the start of the

financial year and lower than the growth rate of 6.2 percent

and 9.3 percent achieved in the financial years 2011-2012

and 2010-2011, respectively.

During the financial year, especially in the first half, almost all

macroeconomic factors continued to deteriorate. Despite

a sharp slowdown in growth and Reserve Bank of India’s

(RBI) tough stance to keep interest rates high, the inflation,

especially the Consumer Price Index (CPI), remained in

double digits for almost the entire year. The negative real

rate of return pulled savings away from productive financial

assets into unproductive physical assets like gold, whic

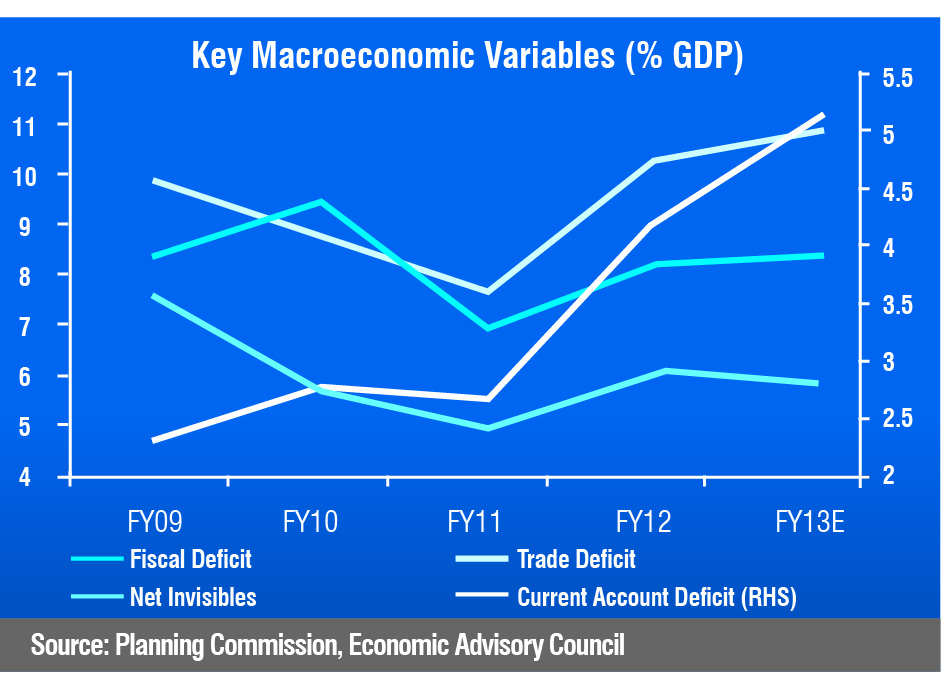

led to an increase in the current account deficit. During the

year, India witnessed one of its highest current account

deficits with Q3FY13’s current account deficit widening

to 6.7 per cent of the GDP which is way above the often

stated comfortable level of 3 per cent of the GDP. Other

factors like high fiscal deficit and low corporate profitability

also contributed to the reduction in savings and increase in

the current account deficit.

During the year, the merchandise trade deficit increased

further from 10.2 percent to 10.9 percent of the GDP due to a decline in exports.

On the positive side, the government took a number of bold steps during the second half of the financial year that are expected to have a positive impact on the economy.

The government’s commitment to meet its guidance on the fiscal deficit number; consistently reduce fiscal deficit

by cutting subsidies and hence free up capital for the

more productive private sector; take constructive steps to

boost investor confidence and there-by to ensure sufficient

external funding to meet its current account deficit and

stability of rupee over the short-term, should gradually get the economy back into a higher growth momentum.

_1.png)